As filed with the Securities and Exchange Commission on February 6, 2009.

(RULE 14A-101)

14a-101)INFORMATION REQUIRED IN PROXY STATEMENT

FILE NUMBER 811-00560

PROXY STATEMENT PURSUANT TO SECTION 14(A) OF THE SECURITIESProxy Statement Pursuant to Section 14(a) of the Securities

EXCHANGE ACT OFExchange Act of 1934 (AMENDMENT NO. )

þ(Amendment No. ______)Filed by the Registrant

oxFiled by a Party other than the Registrant

¨Check the appropriate box:

o Preliminary Proxy Statement

þ Definitive Proxy Statement

o Definitive Additional Materials

o Soliciting Material Pursuant to Rule 14a-11(c) or Rule 14a-12

| ¨ | Preliminary Proxy Statement |

| ¨ | Confidential, for Use of the Commission Only (as permitted by Rule 14a-6(e)(2)) |

| x | Definitive Proxy Statement |

| ¨ | Definitive Additional Materials |

| ¨ | Soliciting Material Pursuant to §240.14a-12 |

JOHN HANCOCK INVESTMENT TRUST

(Name of Registrant as Specified in Its Charter)

JOHN HANCOCK INVESTMENT TRUST

(Name of Person(s) Filing Proxy Statement)

Payment of filing fee (checkFiling Fee (Check the appropriate box):

| x | No fee required. |

| |

| ¨ | Fee computed on table below per Exchange Act Rules 14a-6(i)(1) and 0-11. |

| |

| (1) | Title of each class of securities to which transaction applies: |

| | |

| (2) | Aggregate number of securities to which transaction applies: |

| | |

| (3) | Per unit price or other underlying value of transaction computed pursuant to Exchange Act Rule 0-11

(Set forth the amount on which the filing fee is calculated and state how it was determined): |

| | |

| (4) | Proposed maximum aggregate value of transaction: |

| | |

| (5) | Total fee paid: |

| | |

| ¨ | Fee paid previously with preliminary materials. |

| | |

| ¨ | Check box if any part of the fee is offset as provided by Exchange Act Rule 0-11(a)(2) and identify the filing for which the offsetting fee was paid previously. Identify the previous filing by registration statement number, or the Form or Schedule and the date of its filing. |

| | |

| (1) | Amount Previously Paid: |

| | |

| (2) | Form, Schedule or Registration Statement No.: |

| | |

| (3) | Filing Party: |

| | |

| (4) | Date Filed: |

o $125 per Exchange Act Rules 0-11(c) (1) (ii), 14a-6 (i) (1), or

14a-6 (i) (2) or Item 22(a) (2) or schedule 14A (sent by wire transmission).

o Fee paid previously with preliminary materials.

Important Information

March 2, 2017February 6, 2009

John Hancock Bond Trust

John Hancock California Tax-Free Income Fund

John Hancock Capital Series

John Hancock Current Interest

John Hancock Equity Trust

John Hancock Investment Trust

John Hancock Investment Trust II

John Hancock Investment Trust III

John Hancock Municipal Securities Trust

John Hancock Series Trust

John Hancock Sovereign Bond Fund

John Hancock Strategic Series

John Hancock Tax-Exempt Series Fund

John Hancock World Fund

Please vote today.

Dear Shareholder:

shareholder:I am writing to ask for your assistance with an important matter involvingvote on the enclosed proxy proposals. From time to time, the management team at John Hancock Investments seeks to update a fund’s fundamental investment policies (which requires shareholder approval), often to give a fund greater flexibility in the future regarding what it can invest in and to what degree. This is the case for your investmentfund, John Hancock Fundamental Large Cap Core Fund, and implementing these changes requires approval by both the Board of Trustees and fund shareholders. We recently recommended the enclosed changes to the Board, and the Board agreed that these amendments were in one or morethe best interests of shareholders.

Some of the proposals, which are detailed in the following pages, modernize and streamline the fund’s investment portfolios (the “Funds”)restrictions. As a practical matter, these amendments do not substantively change the restrictions, but rather provide the flexibility to accommodate potential future legal and regulatory developments. Other proposals eliminate restrictions that were previously required under state “blue sky” regulations that are no longer in effect. In order for these changes to take effect, we need your approval as a registered shareholder of the trusts listed above (the “Trusts”). You are being askedfund. Please read the enclosed proxy statement, and take the time to vote using any of the methods detailed below.

Thank you for choosing John Hancock Investments and for giving these important proposals your attention.

How to vote

A special shareholder meeting to vote on several proposedthese proposals has been scheduled for May 15, 2017, at the offices of John Hancock Investments, 601 Congress Street, Boston, Massachusetts. While you may attend the meeting in person,voting today will save on the potential cost of future mailings required to obtain shareholder votes.You may vote your shares by proxy in one of three ways:

Online:www.proxyvote.com

Phone:Call 1-800-690-6903

Mail:by returning the enclosed proxy card(s)

Sincerely,

/s/ Andrew G. Arnott

Andrew G. Arnott

President and CEO

John Hancock Investments

March 2, 2017

Please vote today.

Dear shareholder:

I am writing to ask for your vote on the enclosed proxy proposals. From time to time, the management team at John Hancock Investments seeks to update a fund’s fundamental investment policies (which requires shareholder approval), often to give a fund greater flexibility in the future regarding what it can invest in and to what degree. This is the case for your fund, John Hancock Fundamental Large Cap Core Fund, and implementing these changes affectingrequires approval by both the Funds. To considerBoard of Trustees and fund shareholders. We recently recommended the enclosed changes to the Board, and the Board agreed that these amendments were in the best interests of shareholders.

Some of the proposals, which are detailed in the following pages, modernize and streamline the fund’s investment restrictions. As a practical matter, these amendments do not substantively change the restrictions, but rather provide the flexibility to accommodate potential future legal and regulatory developments. Other proposals eliminate restrictions that were previously required under state “blue sky” regulations that are no longer in effect. In order for these changes to take effect, we need your approval as a registered shareholder of the fund. Please read the enclosed proxy statement, and take the time to vote using any of the methods detailed below.

Thank you for choosing John Hancock Investments and for giving these important proposals your attention.

How to vote

A special shareholder meeting to vote on these proposed changes, proposals has been scheduled for May 15, 2017, at the offices of John Hancock Investments, 601 Congress Street, Boston, Massachusetts. While you may attend the meeting in person,voting today will save on the potential cost of future mailings required to obtain shareholder votes.You may vote your shares by proxy in one of three ways:

Online:by visiting the website on your proxy card(s) and entering your control number

Phone:by calling the number listed on your proxy card(s)

Mail:by returning the enclosed proxy card(s)

Sincerely,

/s/ Andrew G. Arnott

Andrew G. Arnott

President and CEO

John Hancock Investments

JOHN HANCOCK FUNDAMENTAL LARGE CAP CORE FUND

a Special Joint Meetingseries of ShareholdersJOHN HANCOCK INVESTMENT TRUST

601 Congress Street

Boston, Massachusetts 02210

NOTICE OF SPECIAL MEETING OF SHAREHOLDERS

To the shareholders of John Hancock Fundamental Large Cap Core Fund (the “Fund”):

Notice is hereby given that a special meeting of shareholders of the TrustsFund will be held at 601 Congress Street, Boston, Massachusetts 02210, onApril 16, 2009,Monday, May 15, 2017, at 2:00 p.m.P.M., Eastern Time(the “Meeting”). We encourage you to read the attached materials in their entirety.

The enclosed proxy statement sets forth six proposals that you are being asked to vote on. The first proposal, a routine item, concerns the election of trustees. Routine items make no fundamental or material changes to a Fund’s investment objectives, policies or restrictions, or to the investment management contract. The other proposals are not considered routine items. All six are summarized below.

The following is an overview of the proposals on which you are being asked to vote. Please note that none of these proposals is expected to have any material effect on the manner in which any Fund is managed or on its current investment objective, nor are they related to the current state of the financial markets. You will find a detailed explanation of each proposal in the enclosed proxy materials.

You are being asked to approve several proposals:

You are being asked to elect eleven Trustees as members of the Board of Trustees of each Trust (a “Board”).

| |

(2) | New Form of Advisory Agreement |

You are being asked to approve a new form of Advisory Agreement between each Trust and John Hancock Advisers, LLC (“JHA” or the “Adviser”). The purpose of this proposal is to streamline the advisory agreements across the John Hancock Fund Complex, primarily to clarify that the new Agreement covers only investment advisory services. Consistency in operational procedures across the John Hancock Fund Complex will speed processes and minimize transaction error. These benefits contribute to a goal of maintaining, even reducing, operational costs. Restricting the new form of Advisory Agreement to investment advisory services will facilitate the Adviser’s ability to manage those services that are “non-investment” in nature.

The new form of Advisory Agreement will not result in any change in advisory fee rates or the level or quality of advisory services provided to the Funds, and will not materially increase the Funds’ overall expense ratios.Other details and impacts of this proposal are described in the accompanying proxy statement.

| |

(3) | Revisions to, or Elimination of, Fundamental Investment Policies and Restrictions |

You are being asked to approve various amended and restated fundamental investment restrictions for the Funds, as described in the proxy statement. This proposal is intended to conform and standardize many of the investment restrictions that apply to the Funds and other funds in the John Hancock Fund Complex. Standardizing the investment restrictions is expected to facilitate more effective management of the Funds by the Adviser and the subadvisers, enhance monitoring compliance with applicable restrictions and eliminate conflicts among comparable restrictions resulting from minor variations in their terms. The proposed amendments are not expected to have any material effect on the manner in which any Fund is managed or on its current investment objective. In addition, you are being asked to approve the elimination of fundamental investment restrictions for various Funds, which had been required under state “blue sky” regulations that are no longer in effect.

| |

(4) | Proposal to Change CertainRule 12b-1 Plans |

You are being asked to approve an amendment to changeRule 12b-1 Plans for certain classes of the Funds from “reimbursement” to “compensation” Plans. This could be expected to result in greater flexibility and ease of administration and accounting with respect to distribution-related payments and expenses.

| |

(5) | Proposal adopting a Manager of Managers Structure |

You are being asked to approve a “manager of managers” structure for certain Funds. This structure would allow JHA, with the approval of the applicable Board, to replace a Fund’s subadviser or materially amend the Fund’s investment subadvisory agreement without obtaining shareholder approval, subject to certain conditions. This effectively would allow JHA to hire and replace subadvisers to the Funds, subject to Board approval but without a Fund having to incur the cost and delay of holding a shareholder meeting to approve a new (or materially amend a current) investment subadvisory agreement for that Fund. Shareholders would, however, be notified of any changes to a Fund’s subadvisers.

| |

(6) | Revision to Merger Approval Requirements |

You are being asked to approve an amendment to modernize each Trust’s Declaration of Trust, as described in the proxy statement. This proposal is intended to permit mergers of affiliated Funds without a shareholder vote in certain circumstances to reduce the need for affiliated Funds to incur the expense of soliciting proxies when a merger would not raise significant issues for shareholders. The amendment will provide the Trustees with increased flexibility to react more quickly to new developments and changes in competitive and regulatory conditions and, as a consequence, may result in Funds that operate more efficiently and economically.

We Need Your Vote of Approval

After careful consideration, each Board has unanimously approved each of the applicable proposals and recommends that shareholders vote “FOR” their approval, but the final approval requires your vote. The enclosed proxy statement, which I strongly encourage you to read before voting, contains further explanation and important details of the proposals.

Your Vote Matters!

You are being asked to approve these proposals. No matter how large or small your Fund holdings, your vote is extremely important. After you review the proxy materials, please submit your vote promptly to help us avoid the need for additional mailings. For your convenience, you may vote one of three ways: via telephone by calling the number listed on your proxy card, via mail by returning the enclosed voting card or via the Internet by visiting www.jhfunds.com/proxy and selecting the appropriate Fund. I am confident that the proposed changes will help us better serve all of the Funds’ shareholders. If you have questions, please call a John Hancock Funds Customer Service Representative at1-800-225-5291 between 8:00 a.m. and 7:00 p.m., Eastern Time. I thank you for your time and your prompt vote on these matters.

Sincerely,

Keith F. Hartstein

Chief Executive Officer

John Hancock Funds, LLC, 601 Congress Street, Boston, Massachusetts 02210, Member FINRA, SIPC • John Hancock Advisers, LLC • John Hancock Signature Services, Inc.

JOHN HANCOCK BOND TRUST

JOHN HANCOCK CALIFORNIA TAX-FREE INCOME FUND

JOHN HANCOCK CAPITAL SERIES

JOHN HANCOCK CURRENT INTEREST

JOHN HANCOCK EQUITY TRUST

JOHN HANCOCK INVESTMENT TRUST

JOHN HANCOCK INVESTMENT TRUST II

JOHN HANCOCK INVESTMENT TRUST III

JOHN HANCOCK MUNICIPAL SECURITIES TRUST

JOHN HANCOCK SERIES TRUST

JOHN HANCOCK SOVEREIGN BOND FUND

JOHN HANCOCK STRATEGIC SERIES

JOHN HANCOCK TAX-EXEMPT SERIES FUND

JOHN HANCOCK WORLD FUND

(the “Trusts”)

601 Congress Street

Boston, Massachusetts 02210

NOTICE OF SPECIAL JOINT MEETING OF SHAREHOLDERS

To the Shareholders of the Trusts:

Notice is hereby given that a Special Joint Meeting of Shareholders of all of the investment portfolios (the “Funds”) of the Trusts will be held at 601 Congress Street, Boston, Massachusetts 02210, onApril 16, 2009 at 2:00 p.m., Eastern Time(the “Meeting”). A Proxy Statement, which provides information about the purposes of the Meeting, is included with this notice. The Funds involved in the Meeting are listed on the front cover of the Proxy Statement. The Meeting will be held for the following purposes:

| | |

| Proposal 1 | | Election of eleven Trustees as members of the Board of Trustees of each of the Trusts. |

| | All shareholders of each Trust will vote separately on Proposal 1. |

Proposal 2 | | Approval of a new form of Advisory Agreement between each Trust and John Hancock Advisers, LLC. |

| | Shareholders of each Fund will vote separately on Proposal 2. |

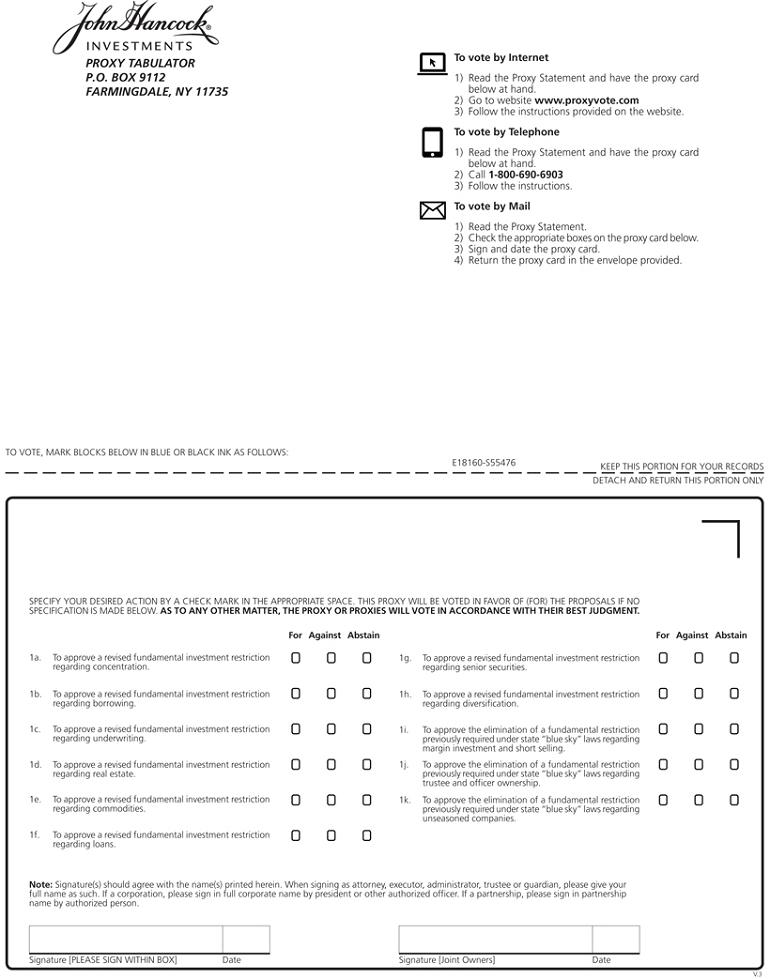

Proposal 3 | | Approval ofTo approve revised fundamental investment restrictions regarding: |

| | (a) Concentration; | Concentration |

| | (b) Diversification; | Borrowing |

| | (c) Underwriting; | Underwriting |

| | (e) Loans; and | Commodities |

| | (f) Senior securities. | Loans |

| | Shareholders of each Fund will vote separately on Proposal 3(a). |

| | Shareholders of each Fund (except California Tax-Free Income Fund, Greater China Opportunities Fund, Health Sciences Fund, High Yield Municipal Bond Fund, International Classic Value Fund and U.S. Global Leaders Growth Fund) will vote separately on Proposal 3(b). |

| | Shareholders of each Fund will vote separately on each of Proposals 3(c) through 3(f). |

| | Approval of elimination of fundamental restrictions previously required under state “blue sky” laws: |

| | (g) Oil, gas | Senior Securities |

To approve the elimination of fundamental restrictions previously required under state “blue sky” laws regarding:

| (i) | Margin Investment and mineral programs;Short Selling |

| (j) | (h) Investment to exercise control; |

| | (i) Trustee and officer ownership;Officer Ownership |

| (k) | (j) Margin investment; short selling;Unseasoned Companies |

i

Shareholders of the Fund will vote separately on each of Proposals 1(a) through (k). | | |

| | (k) Restricted securities; |

| | (l) Pledging assets; |

| | (m) Unseasoned companies; |

| | (n) Loans to Trust officers and Trustees; and |

| | (o) Warrants. |

| | Shareholders of Government Income Fund and Money Market Fund will vote separately on each of Proposals 3(g) and 3(h). |

| | Shareholders of Government Income Fund, Investment Grade Bond Fund, Large Cap Equity Fund and Money Market Fund will vote separately on Proposal 3(i). |

| | Shareholders of Government Income Fund, Investment Grade Bond Fund, Large Cap Equity Fund, Money Market Fund and Regional Bank Fund will vote separately on Proposal 3(j). |

| | Shareholders of Government Income Fund and Money Market Fund will vote separately on Proposal 3(k). |

| | Shareholders of Balanced Fund, Bond Fund, Health Sciences Fund, Massachusetts Tax-Free Income Fund, New York Tax-Free Income Fund and Strategic Income Fund will vote separately on Proposal 3(l). |

| | Shareholders of Large Cap Equity Fund will vote separately on each of Proposals 3(m) and 3(n). |

| | Shareholders of Regional Bank Fund will vote separately on Proposal 3(o). |

Proposal 4 | | Approval of amendments changingRule 12b-1 Plans for certain classes of the Funds from “reimbursement” to “compensation” Plans. |

| | Applies to all Funds having Class A, Class B, Class C, Class R, Class R1, Class R2, Class R3, Class R4 and/or Class R5 shares. Shareholders of each such Fund will vote separately, and individually by share class, on Proposal 4. |

Proposal 5 | | Proposal adopting a manager of managers structure. |

| | Shareholders of each Fund (except Classic Value Fund II, International Classic Value Fund and Small Cap Fund) will vote separately on Proposal 5. |

Proposal 6 | | Revision to merger approval requirements. |

| | All shareholders of each Trust will vote separately on Proposal 6. |

Any other business that may properly come before the Meeting or any adjournment of the Meeting.

EachThe Board of Trustees of the Trusts recommends that shareholdersyou vote “FOR” all the Proposals.

FOR Proposals 1(a) through (k).Each shareholder of record atof the Fund as of the close of business on January 23, 2009February 27, 2017, is entitled to receive notice of, and to vote at, the Meeting.

Meeting and at any adjournment thereof.

Whether or not you expect to attend the Meeting, please complete and return the enclosed proxy card in the accompanying envelope. No postage is necessary if mailed in the United States.

Important Notice Regarding the Availability of Proxy Materials for

the Shareholder Meeting to beBe Held on April 16, 2009.May 15, 2017:

The proxy statementProxy Statement is available at www.accessmyproxy.com.at: www.jhinvestments.com/proxy.

Sincerely,

Thomas M. Kinzler

Secretary

February 6, 2009

| By order of the Board of Trustees, |

| John J. Danello |

| Secretary |

March 2, 2017

Boston, Massachusetts

ii

Your vote is important —- Please vote your shares promptly.

Shareholders are invited to attend the Meeting in person. Valid photo identification may be required to attend the Meeting in person. Any shareholder who does not expect to attend the Meeting is urged to vote by:

| | |

| (i) | completing the enclosed proxy card,card(s), dating and signing it, and returning it in the envelope provided, which needs no postage if mailed in the United States; |

|

| (ii) | following the touch-tone telephone voting instructions found below; or |

|

| (iii) | following the Internet voting instructions found below. |

In order to avoid unnecessary expense, we ask your cooperation in responding promptly, no matter how large or small your holdings may be.

INSTRUCTIONS FOR EXECUTING PROXY CARD

CARDSThe following general rules for executing proxy cards may be of assistance to you and help avoid the time and expense involved in validating your vote if you fail to execute your proxy cardcard(s) properly.

Individual Accounts: Your name should be signed exactly as it appears on the proxy card.

card(s).

Joint Accounts:Either party may sign, but the name of the party signing should conform exactly to a name shown on the proxy card.

card(s).

All other accounts should show the capacity of the individual signing. This can be shown either in the form of the account registration itself or by the individual executing the proxy card.card(s).

INSTRUCTIONS FOR VOTING BY TOUCH-TONE TELEPHONE

Read the enclosed Proxy Statement, and have your proxy cardcard(s) handy.

Call the toll-free number indicated on your proxy card.

card(s).Enter the control number found on the front of your proxy card. card(s).

Follow the recorded instructions to cast your vote.

INSTRUCTIONS FOR VOTING BY INTERNET

Read the enclosed Proxy Statement, and have your proxy cardcard(s) handy.

Go to the Web site on the proxy card.

card(s).Enter the “control number”control number found on the front of your proxy card.

card(s).Follow the instructions on the Web site. Please call the toll-free number indicated on your proxy card if you have any problems.

iii

JOHN HANCOCK BOND TRUST

JOHN HANCOCK CALIFORNIA TAX-FREE INCOME FUND

JOHN HANCOCK CAPITAL SERIES

JOHN HANCOCK CURRENT INTEREST

JOHN HANCOCK EQUITY TRUST

JOHN HANCOCK INVESTMENT TRUST

JOHN HANCOCK INVESTMENT TRUST II

JOHN HANCOCK INVESTMENT TRUST III

JOHN HANCOCK MUNICIPAL SECURITIES TRUST

JOHN HANCOCK SERIES TRUST

JOHN HANCOCK SOVEREIGN BOND FUND

JOHN HANCOCK STRATEGIC SERIES

JOHN HANCOCK TAX-EXEMPT SERIES FUND

JOHN HANCOCK WORLD FUND

(the “Trusts”)

PROXY STATEMENT

SPECIAL JOINT MEETING OF SHAREHOLDERS

TO BE HELD APRIL 16, 2009

| | |

JOHN HANCOCK BOND TRUSTTABLE OF CONTENTS | | JOHN HANCOCK INVESTMENT TRUST II |

John Hancock Government Income Fund | | John Hancock Financial Industries Fund |

John Hancock High Yield Fund | | John Hancock Regional Bank Fund |

John Hancock Investment Grade Bond Fund | | John Hancock Small Cap Equity Fund |

JOHN HANCOCK CALIFORNIA TAX-FREE | | JOHN HANCOCK INVESTMENT TRUST III |

INCOME FUND

| | John Hancock Greater China Opportunities Fund |

John Hancock California Tax-Free Income Fund | | JOHN HANCOCK MUNICIPAL SECURITIES |

JOHN HANCOCK CAPITAL SERIES | | TRUST |

John Hancock Classic Value Fund | | John Hancock High Yield Municipal Bond Fund |

John Hancock Classic Value Fund II | | John Hancock Tax-Free Bond Fund |

John Hancock International Classic Value Fund | | JOHN HANCOCK SERIES TRUST |

John Hancock Large Cap Select Fund | | John Hancock Mid Cap Equity Fund |

John Hancock U.S. Global Leaders Growth Fund | | John Hancock Global Real Estate Fund |

JOHN HANCOCK CURRENT INTEREST | | JOHN HANCOCK SOVEREIGN BOND FUND |

John Hancock Money Market Fund | | John Hancock Bond Fund |

JOHN HANCOCK EQUITY TRUST | | JOHN HANCOCK STRATEGIC SERIES |

John Hancock Small Cap Fund | | John Hancock Strategic Income Fund |

JOHN HANCOCK INVESTMENT TRUST | | JOHN HANCOCK TAX-EXEMPT SERIES FUND |

John Hancock Balanced Fund | | John Hancock Massachusetts Tax-Free Income |

John Hancock Global Opportunities Fund | | Fund |

John Hancock Large Cap Equity Fund | | John Hancock New York Tax-Free Income Fund |

John Hancock Small Cap Intrinsic Value Fund | | JOHN HANCOCK WORLD FUND |

John Hancock Sovereign Investors Fund | | John Hancock Health Sciences Fund |

iv

The following table summarizes which Funds (and share classes) are being asked to vote on a particular Proposal.

| | | | | | |

Proposal | | | Funds | | | Classes |

1 | | | All Funds | | | All Classes |

| | | | | | |

2 | | | All Funds | | | All Classes |

| | | | | | |

3(a) | | | All Funds | | | All Classes |

| | | | | | |

3(b) | | | Balanced Fund

Bond Fund

Classic Value Fund

Classic Value Fund II

Financial Industries Fund

Global Opportunities Fund

Global Real Estate Fund

Government Income Fund

High Yield Fund

Investment Grade Bond Fund

Large Cap Equity Fund

Large Cap Select Fund

Massachusetts Tax-Free Income Fund

Mid Cap Equity Fund

Money Market Fund

New York Tax-Free Income Fund

Regional Bank Fund

Small Cap Equity Fund

Small Cap Fund

Small Cap Intrinsic Value Fund

Sovereign Investors Fund

Strategic Income Fund

Tax-Free Bond Fund | | | All Classes |

| | | | | | |

3(c) to 3(f) | | | All Funds | | | All Classes |

| | | | | | |

3(g) and 3(h) | | | Government Income Fund

Money Market Fund | | | All Classes |

| | | | | | |

3(i) | | | Government Income Fund

Investment Grade Bond Fund

Large Cap Equity Fund

Money Market Fund | | | All Classes |

| | | | | | |

3(j) | | | Government Income Fund

Investment Grade Bond Fund

Large Cap Equity Fund

Money Market Fund

Regional Bank Fund | | | All Classes |

| | | | | | |

3(k) | | | Government Income Fund

Money Market Fund | | | All Classes |

| | | | | | |

3(l) | | | Balanced Fund

Bond Fund

Health Sciences Fund

Massachusetts Tax-Free Income Fund

New York Tax-Free Income Fund

Strategic Income Fund | | | All Classes |

| | | | | | |

3(m) and 3(n) | | | Large Cap Equity Fund | | | All Classes |

| | | | | | |

3(o) | | | Regional Bank Fund | | | All Classes |

| | | | | | |

v

| | | | | | |

Proposal | | | Funds | | | Classes |

4 | | | All Funds | | | A, B, and C |

| | | | | | |

| | |

| Proposal 1 ─ Approval of REVISion or elimination of FUNDAMENTAL RESTRICTIONS | Balanced Fund

Bond Fund

Classic Value Fund

Classic Value Fund II

Large Cap Select Fund

Small Cap Equity Fund

Sovereign Investors Fund

Strategic Income Fund

U.S. Global Leaders Growth Fund | | | R12 |

| | |

| Introduction | 2 |

| Proposal 1(a) — Amended Fundamental Restriction Relating to Concentration | 3 |

| Proposal 1(b) — Amended Fundamental Restriction Relating to Borrowing | 4 |

| Proposal 1(c) — Amended Fundamental Restriction Relating to Underwriting | 5 |

| Proposal 1(d) — Amended Fundamental Restriction Relating to Real Estate | 6 |

| Proposal 1(e) — Amended Fundamental Restriction Relating to Commodities | 6 |

| Proposal 1(f) — Amended Fundamental Restriction Relating to Loans | 7 |

| Proposal 1(g) — Amended Fundamental Restriction Relating to Senior Securities | 8 |

| Proposal 1(h) — Amended Fundamental Restriction Relating to Diversification | 9 |

| Proposal 1(i) — Elimination of Fundamental Restriction Relating to Margin Investment and Short Selling | 10 |

| Proposal 1(j) — Elimination of Fundamental Restriction Relating to Trustee and Officer Ownership | 11 |

| Proposal 1(k) — Elimination of Fundamental Restriction Relating to Unseasoned Companies | 11 |

| | |

| miscellaneous | | | Balanced Fund | | | R, R2, R3, R4, and R511 |

| | |

| Voting Procedures | 11 |

| Telephone Voting | 12 |

| Internet Voting | 13 |

| Shareholders Sharing the Same Address | 13 |

| Other Matters | 13 |

| | |

5Appendix A | | | Balanced Fund

Bond Fund

California Tax-Free Income Fund

Classic Value Fund

Financial Industries Fund

Global Opportunities Fund

Global Real Estate Fund

Government Income Fund

Greater China Opportunities Fund

Health Sciences Fund

High Yield Fund

High Yield Municipal Bond Fund

Investment Grade Bond Fund

Large Cap Equity Fund

Large Cap Select Fund

Massachusetts Tax-Free Income Fund

Mid Cap Equity Fund

Money Market Fund

New York Tax-Free Income Fund

Regional Bank Fund

Small Cap Equity Fund

Small Cap Intrinsic Value Fund

Sovereign Investors Fund

Strategic Income Fund

Tax-Free Bond Fund

U.S. Global Leaders Growth Fund | | | All Classes |

| | | | | | |

6 | | | All Funds | | | All Classes |

| | | | | | A-1 |

vi

TABLE OF CONTENTS

| | | | |

| | | 1 | |

| | | 2 | |

| | | 14 | |

| | | 22 | |

| | | 23 | |

| | | 26 | |

| | | 28 | |

| | | 30 | |

| | | 31 | |

| | | 33 | |

| | | 35 | |

| | | 36 | |

| | | 36 | |

| | | 37 | |

| | | 38 | |

| | | 39 | |

| | | 39 | |

| | | 40 | |

| | | 40 | |

| | | 41 | |

| | | 49 | |

| | | 51 | |

| | | 52 | |

| | | 54 | |

| | | 57 | |

| | | 58 | |

| | | A-1 | |

| | | B-1 | |

| | | C-1 | |

| | | D-1 | |

| | | E-1 | |

| | | F-1 | |

vii

JOHN HANCOCK BOND TRUSTFUNDAMENTAL LARGE CAP CORE FUND,

JOHN HANCOCK CALIFORNIA TAX-FREE INCOME FUND

JOHN HANCOCK CAPITAL SERIES

JOHN HANCOCK CURRENT INTEREST

JOHN HANCOCK EQUITY TRUST

a series of JOHN HANCOCK INVESTMENT TRUST

JOHN HANCOCK INVESTMENT TRUST II

JOHN HANCOCK INVESTMENT TRUST III

JOHN HANCOCK MUNICIPAL SECURITIES TRUST

JOHN HANCOCK SERIES TRUST

JOHN HANCOCK SOVEREIGN BOND FUND

JOHN HANCOCK STRATEGIC SERIES

JOHN HANCOCK TAX-EXEMPT SERIES FUND

JOHN HANCOCK WORLD FUND

(the “Trusts”)

601 Congress Street

Boston, Massachusetts 02210

PROXY STATEMENT

SPECIAL JOINT MEETING OF SHAREHOLDERS

TO BE HELD APRIL 16, 2009

ON MAY 15, 2017This Proxy Statement contains the information that a shareholder should know before voting on the proposals described in the notice.The Fund will furnish, without charge, a copy of its Annual Report and/or Semiannual Report to any shareholder upon request by writing to the Fund at 601 Congress Street, Boston, Massachusetts 02210 or by calling 1-800-225-5291.

INTRODUCTION

This Proxy Statement is being furnished in connection with the solicitation of proxies by eachthe Board of Trustees (the “Board” or “Trustees”) of eachJohn Hancock Investment Trust of proxies to be used(the “Trust”) for use at a Special Joint Meetingthe special meeting of shareholders of John Hancock Fundamental Large Cap Core Fund (the “Fund”), a series of the Trusts toTrust. The special meeting will be held at 601 Congress Street, Boston, Massachusetts 02210, onApril 16, 2009 Monday, May 15, 2017, at 2:00 p.m.P.M., Eastern Time(the (the “Meeting”). PursuantThe Board is soliciting proxies from shareholders with respect to the Agreementproposals set forth in the accompanying notice.

The following table summarizes the proposals.

| Proposal Number | | Description of Proposal |

| | |

| Proposal 1(a) | | To approve a revised fundamental investment restriction regarding concentration. |

| | |

| Proposal 1(b) | | To approve a revised fundamental investment restriction regarding borrowing. |

| | |

| Proposal 1(c) | | To approve a revised fundamental investment restriction regarding underwriting. |

| | |

| Proposal 1(d) | | To approve a revised fundamental investment restriction regarding real estate. |

| | |

| Proposal 1(e) | | To approve a revised fundamental investment restriction regarding commodities. |

| | |

| Proposal 1(f) | | To approve a revised fundamental investment restriction regarding loans. |

| | |

| Proposal 1(g) | | To approve a revised fundamental investment restriction regarding senior securities. |

| | |

| Proposal 1(h) | | To approve a revised fundamental investment restriction regarding diversification. |

| | |

| Proposal 1(i) | | To approve the elimination of a fundamental restriction previously required under state “blue sky” laws regarding margin investment and short selling. |

| | |

| Proposal 1(j) | | To approve the elimination of a fundamental restriction previously required under state “blue sky” laws regarding trustee and officer ownership. |

| | |

| Proposal 1(k) | | To approve the elimination of a fundamental restriction previously required under state “blue sky” laws regarding unseasoned companies. |

The definitive Proxy Statement and Declarationproxy card are intended to be first mailed to shareholders on or about March 15, 2017.

The Fund’s Advisor, Administrator, Distributor, and Subadvisor

John Hancock Advisers, LLC (the “Advisor”), 601 Congress Street, Boston, Massachusetts, 02210, serves as the Fund’s investment advisor and administrator. An affiliate of Trustthe Advisor, John Hancock Funds, LLC, 601 Congress Street, Boston, Massachusetts 02210, serves as the Fund’s distributor. Another affiliate of each Trust (the “Declarationthe Advisor, John Hancock Asset Management a division of Trust”), eachManulife Asset Management (US) LLC, 197 Clarendon Street, Boston, Massachusetts 02116, serves as the Fund’s subadvisor.

Record Ownership

The Board has designated January 23, 2009fixed the close of business on February 27, 2017 as the record date for determining shareholders eligible to vote at the Meeting (the “Record Date”). All shareholders of record at the close of business on the Record Date are entitled to one vote for each share (and fractional votes for fractional shares) on all business of the Meeting or any adjournment of the Meeting. On the Record Date, 96,259,788 shares of beneficial interest of Trusts held. This Proxy Statement is first being sent to shareholders on or about February 6, 2009.

Each of the Trusts is an open-end management investment company, commonly known as a mutual fund, registered under the Investment Company Act of 1940, as amended (the “1940 Act”). The shares of each of the 14 Trusts being offered asFund were outstanding.As of the Record Date, were divided into series corresponding to a combined total of 29 portfolios (each a “Fund”). The Funds are named on the cover of this Proxy Statement.

Investment Management. John Hancock Advisers, LLC (“JHA” or the “Adviser”) serves as investment adviser for each Trust and eachnone of the Funds. Pursuant to an investment advisory agreement with each Trust,Trustees beneficially owned individually, and the Adviser is responsible for, among other things, administeringTrustees and executive officers of the business and affairsFundas a group did not beneficially own, in excess of one percent of the Funds and selecting, contracting with, compensating and monitoring the performanceoutstanding shares of the investment subadvisersFund. Information regarding shareholders that manage the investment and reinvestmenthold 5% or more of the assetsFund’s shares of the Funds pursuant to subadvisory agreements with the Adviser. JHARecord Date is registered as an investment adviser under the Investment Advisers Act of 1940, as amended (the “Advisers Act”). Each of the subadvisers to the Funds is also registered as an investment adviser under the Advisers Act or is exempt from such registration.

The Distributor. John Hancock Funds, LLC (the “Distributor”) serves as each Fund’s distributor.

The offices of JHA and the Distributor are located at 601 Congress Street, Boston, Massachusetts 02210, and their ultimate parent entity is Manulife Financial Corporation (“MFC”), a publicly traded company basedset forth in Toronto, Canada. MFC and its subsidiaries operate as “Manulife Financial” in Canada and Asia and primarily as “John Hancock” in the United States.

1

PROPOSAL 1 — ELECTION OF ELEVEN TRUSTEES AS MEMBERS OF THE BOARD OF TRUSTEES OF EACH TRUST

(All Funds)

Shareholders are being asked to elect each of the individuals listed below (the “Nominees”) as a member of each Board of Trustees of the Trusts. Nine of the Nominees currently are Trustees of each Trust and have served in that capacity continuously since originally elected or appointed. Two of the Nominees, Gregory A. Russo and John G. Vrysen, have not served as Trustees of any Trust, although Mr. Russo currently serves a Trustee of other funds managed by JHA or its affiliates. Because no Trust holds regular annual shareholder meetings, each Nominee, if elected, will hold office until his or her successor is elected and qualified or until he or she dies, retires, resigns, is removed or becomes disqualified.

The persons named as proxies intend, in the absence of contrary instructions, to vote all proxies for the election of the Nominees. If, prior to the Meeting, any Nominee becomes unable to serve for any reason, the persons named as proxies reserve the right to substitute another person or persons of their choice as nominee or nominees. All of the Nominees have consented to being named in this Proxy Statement and to serve if elected. The Trusts know of no reason why any Nominee would be unable or unwilling to serve if elected.

The business and affairs of the Trusts, including those of the Funds, are managed under the direction of the Boards of the Trusts. The following table presents certain information regarding the current Trustees, as well as Nominees who are not currently serving as Trustees, including their principal occupations which, unless specific dates are shown, are of at least five years’ duration. In addition, the table includes information concerning other directorships held by each Nominee in other registered investment companies or publicly traded companies. Information is listed separately for each Nominee who is an “interested person” (as defined in the 1940 Act) of a Trust (the “Interested Trustee”) and the Nominees who are not interested persons of a Trust (the “Independent Trustees”). As stated above, the 14 Trusts have a combined total of 29 separate Funds, and each Trustee oversees all Funds. In addition to the Funds, some Trustees also oversee other funds advised by JHA or JHA’s affiliates (collectively with the Funds, the “John Hancock Fund Complex”). As of December 31, 2008, the John Hancock Fund Complex consisted of 268 funds (including separate series of series mutual funds): John Hancock Trust (“JHT”) (123 funds); John Hancock Funds II (“JHF II”) (95 Funds); John Hancock Funds III (“JHF III”) (12 funds); and 38 other John Hancock funds (including the 29 Funds included in this proxy). Each Nominee’s business address is 601 Congress Street, Boston, Massachusetts 02210.

| | | | | | | | | | | |

Interested Trustees | |

| | | | | | | | | Number of Funds in

| |

| | | | | | | | | John Hancock Fund

| |

Name

| | | Position with

| | | | | | Complex Overseen by

| |

(Birth Year) | | | the Trusts | | | Principal Occupation(s) and Other Directorships During the Past 5 Years | | | Trustee/Nominee | |

James R. Boyle(1)

(1959)

| | | Trustee(2) | | | Executive Vice President, MFC (since 1999); Director and President, John Hancock Variable Life Insurance Company (since 2007); Director and Executive Vice President, John Hancock Life Insurance Company (“JHLICO”) (since 2004); Chairman and Director, JHA, The Berkeley Financial Group, LLC (“The Berkeley Group”) (holding company) and the Distributor (since 2005); Chairman and Director, John Hancock Investment Management Services, LLC (“JHIMS”) (since 2006); Senior Vice President, The Manufacturers Life Insurance Company (U.S.A) (until 2004).(3) | | | | 268 | |

|

John G. Vrysen(1)

(1955)

| | | Nominee

for Trustee

Chief Operating

Officer

(since 2005) | | | Senior Vice President, MFC (since 2006); Director, Executive Vice President and Chief Operating Officer, the Adviser, The Berkeley Group, JHIMS, and the Distributor (since 2007); Chief Operating Officer, JHF, JHF II, JHF III and JHT (since 2007); Director, John Hancock Signature Services, Inc. (“Signature Services”) (since 2005); Chief Financial Officer, the Adviser, The Berkeley Group, MFC Global Investment Management (US), JHIMS, John Hancock Funds, LLC, JHF, JHF II, JHF III and JHT (2005–2007); Vice President, MFC (until 2006). | | | | N/A | |

|

| | |

(1) | | The Trustee is an Interested Trustee due to his position with the Adviser and certain of its affiliates. |

2

| | |

(2) | | Mr. Boyle began service as a Trustee of the various Trusts in different years, as detailed in the table following the biographical information about the Trustees and Nominees. |

|

(3) | | Prior to January 1, 2005, JHLICO (U.S.A.) was named The Manufacturers Life Insurance Company (U.S.A.). |

| | | | | | | | | | | |

Independent Trustees/Nominees | |

| | | | | | | | | Number of Funds in

| |

| | | | | | | | | John Hancock Fund

| |

Name

| | | Position(s) with

| | | Principal Occupation(s) and

| | | Complex Overseen by

| |

(Birth Year) | | | the Trusts | | | Other Directorships During the Past 5 Years | | | Trustee/Nominee | |

James F. Carlin

(1940) | | | Trustee* | | | Director and Treasurer, Alpha Analytical Laboratories (chemical analysis) (since 1985); Part Owner and Treasurer, Lawrence Carlin Insurance Agency, Inc. (since 1995); Part Owner and Vice President, Mone Lawrence Carlin Insurance Agency, Inc. (until 2005); Chairman and CEO, Carlin Consolidated, Inc. (management/investments) (since 1987); Trustee, Massachusetts Health and Education Tax Exempt Trust (1993-2003). | | | | 50 | |

| | | | | | | | | | | |

William H.

Cunningham

(1944) | | | Trustee* | | | Professor, University of Texas, Austin, Texas (since 1971); former Chancellor, University of Texas System and former President of the University of Texas, Austin, Texas; Chairman and CEO, IBT Technologies (until 2001); Director of the following: Hicks Acquisition Company 1, Inc. (since 2007); Hire.com (until 2004), STC Broadcasting, Inc. and Sunrise Television Corp. (until 2001), Symtx, Inc.(electronic manufacturing) (since 2001), Adorno/Rogers Technology, Inc. (until 2004), Pinnacle Foods Corporation (until 2003), rateGenius (until 2003), Lincoln National Corporation (insurance) (since 2006), Jefferson-Pilot Corporation (diversified life insurance company) (until 2006), New Century Equity Holdings (formerly Billing Concepts) (until 2001), eCertain (until 2001), ClassMap.com (until 2001), Agile Ventures (until 2001), AskRed.com (until 2001), Southwest Airlines (since 2000), Introgen (manufacturer of biopharmaceuticals) (since 2000) and Viasystems Group, Inc. (electronic manufacturer) (until 2003); Advisory Director, Interactive Bridge, Inc. (college fundraising) (until 2001); Advisory Director, Q Investments (until 2003); Advisory Director, JP Morgan Chase Bank (formerly Texas Commerce Bank — Austin), LIN Television (until 2008), WilTel Communications (until 2003) and Hayes Lemmerz International, Inc. (diversified automotive parts supply company) (since 2003). | | | | 50 | |

| | | | | | | | | | | |

Deborah Jackson

(1952) | | | Trustee

(since 2008) | | | Chief Executive Officer, American Red Cross of Massachusetts Bay (since 2002); Board of Directors of Eastern Bank Corporation (since 2001); Board of Directors of Eastern Bank Charitable Foundation (since 2001); Board of Directors of American Student Association Corp. (since 1996); Board of Directors of Boston Stock Exchange (2002-2008); Board of Directors of Harvard Pilgrim Healthcare (since 2007). | | | | 50 | |

| | | | | | | | | | | |

Charles L. Ladner

(1938) | | | Trustee* | | | Chairman and Trustee, Dunwoody Village, Inc. (retirement services) (since 2008); Senior Vice President and Chief Financial Officer, UGI Corporation (public utility holding company) (retired 1998); Vice President and Director for AmeriGas, Inc. (retired 1998); Director of AmeriGas Partners, L.P.(gas distribution) (until 1997); Director, EnergyNorth, Inc. (until 1995); Director, Parks and History Association (until 2005). | | | | 50 | |

| | | | | | | | | | | |

3

| | | | | | | | | | | |

Independent Trustees/Nominees | |

| | | | | | | | | Number of Funds in

| |

| | | | | | | | | John Hancock Fund

| |

Name

| | | Position(s) with

| | | Principal Occupation(s) and

| | | Complex Overseen by

| |

(Birth Year) | | | the Trusts | | | Other Directorships During the Past 5 Years | | | Trustee/Nominee | |

Stanley Martin

(1947) | | | Trustee

(since 2008) | | | Senior Vice President/Audit Executive, Federal Home Loan Mortgage Corporation (2004-2006); Executive Vice President/Consultant, HSBC Bank USA (2000-2003); Chief Financial Officer/Executive Vice President, Republic New York Corporation & Republic National Bank of New York (1998-2000); Partner, KPMG LLP (1971-1998). | | | | 50 | |

| | | | | | | | | | | |

Patti McGill Peterson

(1943) | | | Trustee* and

Chairperson

(since 2008) | | | Principal, PMP Globalinc (consulting) (since 2007); Senior Associate, Institute for Higher Education Policy (since 2007); Executive Director, CIES (international education agency) (until 2007); Vice President, Institute of International Education (until 2007); Senior Fellow, Cornell University Institute of Public Affairs, Cornell University (1997-1998); Former President Wells College, St. Lawrence University and the Association of Colleges and Universities of the State of New York. Director of the following: Niagara Mohawk Power Corporation (until 2003); Security Mutual Life (insurance) (until 1997); ONBANK (until 1993). Trustee of the following: Board of Visitors, The University of Wisconsin, Madison (since 2007); Ford Foundation, International Fellowships Program (until 2007); UNCF, International Development Partnerships (until 2005); Roth Endowment (since 2002); Council for International Educational Exchange (since 2003). | | | | 50 | |

| | | | | | | | | | | |

John A. Moore

(1939) | | | Trustee* | | | President and Chief Executive Officer, Institute for Evaluating Health Risks, (nonprofit institution) (until 2001); Senior Scientist, Sciences International (health research) (until 2003); Former Assistant Administrator & Deputy Administrator, Environmental Protection Agency; Principal, Hollyhouse (consulting) (since 2000); Director, CIIT Center for Health Science Research (nonprofit research) (until 2007). | | | | 50 | |

| | | | | | | | | | | |

Steven R. Pruchansky

(1944) | | | Trustee* and

Vice Chairman | | | Chairman and Chief Executive Officer, Greenscapes of Southwest Florida, Inc. (since 2000); Director and President, Greenscapes of Southwest Florida, Inc. (until 2000); Member, Board of Advisors, First American Bank (since 2008); Managing Director, Jon James, LLC (real estate) (since 2000); Director, First Signature Bank & Trust Company (until 1991); Director, Mast Realty Trust (until 1994); President, Maxwell Building Corp. (until 1991). | | | | 50 | |

| | | | | | | | | | | |

Gregory A. Russo

(1949) | | | Nominee for

Trustee | | | Vice Chairman, Risk & Regulatory Matters, KPMG, LLC (“KPMG”) (2002-2006); Vice Chairman, Industrial Markets, KPMG (1998-2002). | | | | 21 | |

| | | | | | | | | | | |

| | |

* | | Except for Ms. Jackson and Mr. Martin, each of whom was appointed as a Trustee of all of the Trusts in 2008, the current Trustees began service as Trustees of the various Trusts in different years, as detailed in the table following the biographical information about the Trustees and Nominees. |

4

Year Each Current Trustee Began Service as a Trustee

(Other than Ms. Jackson and Mr. Martin)

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | Boyle | | | | Carlin | | | | Cunningham | | | | Ladner | | | | McGill Peterson | | | | Moore | | | | Pruchansky | |

| Bond Trust | | | | 2005 | | | | | 1994 | | | | | 1987 | | | | | 1994 | | | | | 2001 | | | | | 2001 | | | | | 1994 | |

| California Tax-Free Income Fund | | | | 2005 | | | | | 1994 | | | | | 1989 | | | | | 1994 | | | | | 2005 | | | | | 2005 | | | | | 1994 | |

| Capital Series | | | | 2005 | | | | | 1992 | | | | | 2005 | | | | | 2004 | | | | | 1996 | | | | | 1996 | | | | | 2005 | |

| Current Interest | | | | 2005 | | | | | 1994 | | | | | 1987 | | | | | 1994 | | | | | 2005 | | | | | 2005 | | | | | 1994 | |

| Equity Trust | | | | 2005 | | | | | 2004 | | | | | 2004 | | | | | 2004 | | | | | 2000 | | | | | 2000 | | | | | 2004 | |

| Investment Trust | | | | 2005 | | | | | 1992 | | | | | 1986 | | | | | 1979 | | | | | 2005 | | | | | 2005 | | | | | 1992 | |

| Investment Trust II | | | | 2005 | | | | | 2005 | | | | | 2005 | | | | | 2004 | | | | | 1993 | | | | | 1991 | | | | | 2005 | |

| Investment Trust III | | | | 2005 | | | | | 2005 | | | | | 2005 | | | | | 2004 | | | | | 1994 | | | | | 1994 | | | | | 2005 | |

| Municipal Securities Trust | | | | 2005 | | | | | 1994 | | | | | 1987 | | | | | 1994 | | | | | 2005 | | | | | 2005 | | | | | 1994 | |

| Series Trust | | | | 2005 | | | | | 1992 | | | | | 1994 | | | | | 1991 | | | | | 2005 | | | | | 2005 | | | | | 1991 | |

| Sovereign Bond | | | | 2005 | | | | | 2005 | | | | | 2005 | | | | | 2004 | | | | | 2001 | | | | | 2001 | | | | | 2005 | |

| Strategic Series | | | | 2005 | | | | | 2005 | | | | | 2005 | | | | | 2004 | | | | | 2001 | | | | | 2001 | | | | | 2005 | |

| Tax-Exempt Series Fund | | | | 2005 | | | | | 2005 | | | | | 2005 | | | | | 2004 | | | | | 1996 | | | | | 1996 | | | | | 2005 | |

| World Fund | | | | 2005 | | | | | 2005 | | | | | 2005 | | | | | 2004 | | | | | 1993 | | | | | 1991 | | | | | 2005 | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Correspondence intended for any of the Nominees may be sent to the attention of the individual Nominee or to a Board at 601 Congress Street, Boston, Massachusetts 02210. All communications addressed to a Board or individual Nominee will be logged and sent to the Board or individual Nominee.

5

Principal Officers Who Are Not Trustees or Nominees

The following table presents information regarding the current principal officers of the Trusts who are neither current Trustees nor Nominees, including their principal occupations which, unless specific dates are shown, are of at least five years’ duration. Each of the officers is an affiliated person of the Adviser. Each such officer’s business address is 601 Congress Street, Boston, Massachusetts02210-2805.

| | | | | | |

| | | Position(s) with

| | | |

Name (Birth Year) | | | Each Trust | | | Principal Occupation(s) During Past 5 Years |

Keith F. Hartstein

(1956) | | | President and Chief Executive Officer

(since 2005) | | | Senior Vice President, MFC (since 2004); Director, President and Chief Executive Officer, JHA, The Berkeley Group, the Distributor (since 2005); Director, MFC Global Investment Management (U.S.), LLC (“MFC Global (U.S.)”) (since 2005); Director, Signature Services (since 2005); President and Chief Executive Officer, JHIMS (since 2006); President and Chief Executive Officer, JHF II, JHF III and JHT; Director, Chairman and President, NM Capital Management, Inc. (since 2005); Chairman, Investment Company Institute Sales Force Marketing Committee (since 2003); Director, President and Chief Executive Officer, MFC Global (U.S.) (2005-2006); Executive Vice President, the Distributor (until 2005). |

Francis V. Knox, Jr.

(1947) | | | Chief Compliance Officer

(since 2005) | | | Vice President and Chief Compliance Officer, JHIMS, JHA and MFC Global (U.S.) (since 2005); Vice President and Chief Compliance Officer, JHF, JHF II, JHF III and JHT (since 2005); Vice President and Assistant Treasurer, Fidelity Group of Funds (until 2004). |

Gordon M. Shone

(1956) | | | Treasurer

(since 2006) | | | Treasurer, JHF (since 2006), JHF II, JHF III and JHT (since 2005); Vice President and Chief Financial Officer, JHT (2003-2005); Senior Vice President, JHLICO (U.S.A.) (since 2001); Vice President, JHIMS and JHA (since 2006). |

Charles A. Rizzo

(1959) | | | Chief Financial Officer (since 2007) | | | Chief Financial Officer, JHF, JHF II, JHF III and JHT (since 2007); Assistant Treasurer, Goldman Sachs Mutual Fund Complex (registered investment companies) (2005-2007); Vice President, Goldman Sachs (2005-2007); Managing Director and Treasurer of Scudder Funds, Deutsche Asset Management (2003-2005). |

Thomas M. Kinzler

(1955) | | | Secretary and Chief Legal Officer

(since 2006) | | | Vice President and Counsel, JHLICO (U.S.A.) (since 2006); Secretary and Chief Legal Officer, the Distributor, JHF II, JHF III and JHT (since 2006); Vice President and Associate General Counsel, Massachusetts Mutual Life Insurance Company (1999-2006); Secretary and Chief Legal Counsel, MML Series Investment Fund (2000-2006); Secretary and Chief Legal Counsel, MassMutual Institutional Funds (2000-2004); Secretary and Chief Legal Counsel, MassMutual Select Funds and MassMutual Premier Funds (2004-2006). |

| | | | | | |

Duties of Trustees; Board Meetings and Board Committees

Each Trust is organized as a Massachusetts business trust. Under each Trust’s Declaration of Trust, the Trustees are responsible for managing the affairs of that Trust, including the appointment of advisers and subadvisers. The Trustees may appoint officers who assist in managing its day-to-day affairs. In 2008, each Fund of John Hancock Capital Series (“Capital Series”), except for the Large Cap Select Fund, and John Hancock Investment Trust (“Investment Trust”) changed its fiscal year end from December 31 to October 31. Accordingly, information in this Proxy Statement relating to the most recent fiscal year for these two Trusts (except as information relates to the Large Cap Select Fund) will be shown through or as of the end of each such Trust’s most recently completed fiscal period (October 31, 2008), as well as for the previous full12-month fiscal year ended December 31, 2007.

6

The Board of each Trust met seven times during each Trust’s last respective12-month fiscal year. The Board of each of Capital Series and Investment Trust met seven times during each such Trust’s respective fiscal period ended October 31, 2008.

During each Trust’s most recent12-month fiscal year and, in the case of Capital Series and Investment Trust, the fiscal period ended October 31, 2008, the Board had four standing committees: the Audit and Compliance Committee, the Contracts/Operations Committee, the Governance Committee and the Investment Performance Committee. Each Committee was comprised entirely of Independent Trustees. In January 2009, each Board’s committee structure was changed to consist of six standing committees. The following discussion relates to the committee structure that was in place through December 2008. The new committee structure is described below under “Revised Committee Structure.”

Audit and Compliance Committee. All of the members of this Committee are independent, and each member is financially literate with at least one having accounting or financial management expertise. Each Board has adopted a written charter for the Committee. This Committee recommends to the full Board independent registered public accounting firms for a Fund, oversees the work of the independent registered public accounting firm in connection with each Fund’s audit, communicates with the independent registered public accounting firm on a regular basis and provides a forum for the independent registered public accounting firm to report and discuss any matters it deems appropriate at any time.

The Audit and Compliance Committee of John Hancock Bond Trust, John Hancock California Tax-Free Income Fund, John Hancock Current Interest, John Hancock Municipal Securities Trust, John Hancock Sovereign Bond Fund, John Hancock Strategic Series and John Hancock Tax-Exempt Series Fund held four meetings during each such Trust’s last respective fiscal year.

The Audit and Compliance Committee of Capital Series, John Hancock Equity Trust, Investment Trust, John Hancock Investment Trust II, John Hancock Investment Trust III, John Hancock Series Trust and John Hancock World Fund held four meetings during each such Trust’s last respective12-month fiscal year. The Audit and Compliance Committee of each of Capital Series and Investment Trust met three times during each such Trust’s respective fiscal period ended October 31, 2008.

Governance Committee. This Committee is comprised of all of the Independent Trustees. This Committee reviews the activities of the other standing committees and makes the final selection and nomination of candidates to serve as Independent Trustees. The Interested Trustees and the officers of each Trust are nominated and selected by the Board.

In reviewing a potential nominee and in evaluating the renomination of current Independent Trustees, this Committee will generally apply the following criteria: (i) the nominee’s reputation for integrity, honesty and adherence to high ethical standards; (ii) the nominee’s business acumen, experience and ability to exercise sound judgments; (iii) a commitment to understand the Funds and the responsibilities of a trustee of an investment company; (iv) a commitment to regularly attend and participate in meetings of a Board and its committees; (v) the ability to understand potential conflicts of interest involving management of the Funds and to act in the interests of all shareholders; and (vi) the absence of a real or apparent conflict of interest that would impair the nominee’s ability to represent the interests of all the shareholders and to fulfill the responsibilities of an Independent Trustee. This Committee does not necessarily place the same emphasis on each criteria and each nominee may not have each of these qualities.

It is the intent of each Governance Committee that at least one Independent Trustee be an “audit committee financial expert” as defined by the Securities and Exchange Commission (the “SEC”).

As long as an existing Independent Trustee continues, in the opinion of the relevant Governance Committee, to satisfy these criteria, each Trust anticipates that the Committee would favor the renomination of an existing Independent Trustee rather than a new candidate. Consequently, while each such Committee will consider nominees recommended by shareholders to serve as Independent Trustees, this Committee may only act upon such recommendations if there is a vacancy on a Board or a committee determines that the selection of a new or additional Independent Trustee is in the best interests of a Fund. In the event that a vacancy arises or a change in Board membership is determined to be advisable, this Committee will, in addition to any

7

shareholder recommendations, consider candidates identified by other means, including candidates proposed by members of this Committee. This Committee may retain a consultant to assist it in a search for a qualified candidate, and has done so recently. Each such Committee has adopted Procedures for the Selection of Independent Trustees, a form of which is attached as Appendix A to this Proxy Statement.

Any shareholder recommendation for Independent Trustee must be submitted in compliance with all of the pertinent provisions ofRule 14a-8 under the Securities Exchange Act of 1934, as amended, to be considered by the Governance Committee. In evaluating a nominee recommended by a shareholder, this Committee, in addition to the criteria discussed above, may consider the objectives of the shareholder in submitting that nominationStatement (“Outstanding Shares and whether such objectives are consistent with the interests of all shareholders. If a Board determines to include a shareholder’s candidate among the slate of nominees, the candidate’s name will be placed on the Fund’s proxy card. If this Committee or a Board determines not to include such candidate among a Board’s designated nominees and the shareholder has satisfied the requirements ofRule 14a-8,Share Ownership”). the shareholder’s candidate will be treated as a nominee of the shareholder who originally nominated the candidate. In that case, the candidate will not be named on the proxy card distributed with a Fund’s Proxy Statement.

Shareholders may communicate with the members of a Board as a group or individually. Any such communication should be sent to a Board or an individual Trusteec/o The Secretary of the relevant Trust at the following address: 601 Congress Street, Boston, Massachusetts02210-2805. The Secretary may determine not to forward any letter to the members of a Board that does not relate to the business of a Fund.

The Governance Committee of John Hancock Bond Trust, John Hancock California Tax-Free Income Fund, John Hancock Current Interest, John Hancock Municipal Securities Trust, John Hancock Sovereign Bond Fund, John Hancock Strategic Series and John Hancock Tax-Exempt Series Fund held two meetings during each such Trust’s last respective fiscal year.

The Governance Committee of Capital Series, John Hancock Equity Trust, Investment Trust, John Hancock Investment Trust II, John Hancock Investment Trust III, John Hancock Series Trust and John Hancock World Fund held one meeting during its last respective12-month fiscal year. The Governance Committee of each of Capital Series and Investment Trust met twice during each such Trust’s respective fiscal period ended October 31, 2008.

Contracts/Operations Committee. Each such Committee oversees the initiation, operation, and renewal of the various contracts between a Fund and other entities. These contracts include advisory and subadvisory agreements, custodial and transfer agency agreements and arrangements with other service providers. Each such Committee held four meetings during each Trust’s last respective12-month fiscal year. The Contracts/Operations Committee of each of Capital Series and Investment Trust met three times during each such Trust’s respective fiscal period ended October 31, 2008.

Investment Performance Committee. Each such Committee monitors and analyzes the performance of a Fund generally, consults with the Adviser as necessary if a Fund requires special attention, and reviews peer groups and other comparative standards as necessary. Each such Committee held four meetings during each Trust’s last respective fiscal year. The Investment Performance Committee of each of Capital Series and Investment Trust met three times during each such Trust’s respective fiscal period ended October 31, 2008.

Revised Committee Structure. Beginning January 2009, each Trust’s committee structure was revised to consist of six committees: the Audit Committee; the Compliance Committee; the Nominating, Governance and Administration Committee (which corresponds to the former Governance Committee); the Investment Performance Committee A and the Investment Performance Committee B (which together correspond to the former Investment Performance Committee); and the Contracts/Operations Committee (which corresponds to the former committee of the same name). In terms of function, other than the separate Audit and Compliance Committees, the current committees operate in the same manner as their predecessor committees.

Audit Committee. The accounting oversight function of this Committee is described above in the discussion of the former Audit and Compliance Committee.

8

Compliance Committee. The primary role of each such Committee is to oversee the activities of the Trust’s Chief Compliance Officer; the implementation and enforcement of the Trust’s compliance policies and procedures; and compliance with the Trust’s and the Independent Trustees’ Codes of Ethics.

The current membership of each committee is set forth below. As Chairperson of the Board, Ms. McGill Peterson is considered anex officiomember of each committee and, therefore, is able to attend and participate in any committee meeting, as appropriate. Prior to January 2009, Ms. Jackson and Messrs. Martin and Russo were not members of any committee.

| | | | | | | | | | |

| | | | Nominating,

| | | | | | |

| | | | Governance and

| | Investment

| | Investment

| | |

Audit | | Compliance | | Administration | | Performance A | | Performance B | | Contracts/Operations |

Mr. Cunningham | | Mr. Carlin | | All Independent | | Ms. Jackson | | Mr. Carlin | | Mr. Ladner |

Ms. Jackson | | Mr. Russo | | Trustees | | Mr. Ladner | | Mr. Cunningham | | Dr. Moore |

Mr. Martin | | | | | | Mr. Martin | | Dr. Moore | | Mr. Pruchansky |

| | | | | | Mr. Pruchansky | | Mr. Russo | | |

Compensation of Trustees

Each Trust pays fees only to its Independent Trustees. Trustees are reimbursed for travel and other out-of-pocket expenses. The following tables show the compensation paid to each Independent Trustee for his or her service as a Trustee for the most recent fiscal years or periods indicated. In these tables, the amount shown for each of Ms. Jackson and Mr. Martin for certain periods is “None” since each of these individuals was appointed to the Board of each Trust after these periods.

Compensation for Fiscal Year Ended October 31, 2008

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | | John

| |

| | | | | | | | | | | | | | | | | | | | | | | | Hancock

| |

| | | | Equity

| | | | Investment

| | | | Investment

| | | | Series

| | | | World

| | | | Fund

| |

| Independent Trustee | | | Trust | | | | Trust II | | | | Trust III | | | | Trust | | | | Fund | | | | Complex* | |

| Carlin | | | $ | 2,060 | | | | $ | 21,249 | | | | $ | 2,453 | | | | $ | 2,205 | | | | $ | 1,558 | | | | $ | 260,834 | |

| Cunningham | | | $ | 1,229 | | | | $ | 12,274 | | | | $ | 1,579 | | | | $ | 1,286 | | | | $ | 941 | | | | $ | 157,500 | |

| Jackson | | | $ | 122 | | | | $ | 2,398 | | | | $ | 194 | | | | $ | 74 | | | | $ | 180 | | | | $ | 34,750 | |

| Ladner | | | $ | 1,229 | | | | $ | 12,274 | | | | $ | 1,579 | | | | $ | 1,286 | | | | $ | 941 | | | | $ | 162,500 | |

| Martin | | | $ | 197 | | | | $ | 3,482 | | | | $ | 339 | | | | $ | 118 | | | | $ | 281 | | | | $ | 51,960 | |

| McGill Peterson | | | $ | 1,229 | | | | $ | 12,275 | | | | $ | 1,579 | | | | $ | 1,286 | | | | $ | 941 | | | | $ | 157,500 | |

| Moore | | | $ | 1,539 | | | | $ | 15,531 | | | | $ | 1,941 | | | | $ | 1,624 | | | | $ | 1,178 | | | | $ | 212,000 | |

| Pruchansky | | | $ | 1,579 | | | | $ | 19,924 | | | | $ | 1,988 | | | | $ | 1,672 | | | | $ | 1,213 | | | | $ | 203,500 | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

9

Compensation for Fiscal Year Ended December 31, 2007 and Fiscal Period ended October 31, 2008

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Independent Trustee | | | Capital Series | | | | Investment Trust | | | | John Hancock Fund Complex* | |

| | | | FYE

| | | | FYE

| | | | FYE

| | | | FYE

| | | | FYE

| | | | FYE

| |

| | | | 12-31-07 | | | | 10-31-08 | | | | 12-31-07 | | | | 10-31-08 | | | | 12-31-07 | | | | 10-31-08 | |

| Carlin | | | $ | 52,172 | | | | $ | 64,455 | | | | $ | 8,446 | | | | $ | 37,201 | | | | $ | 145,250 | | | | $ | 255,834 | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Cunningham | | | $ | 52,181 | | | | $ | 36,282 | | | | $ | 8,448 | | | | $ | 20,289 | | | | $ | 145,250 | | | | $ | 152,500 | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Jackson | | | | None | | | | $ | 6,081 | | | | | None | | | | $ | 6,025 | | | | | None | | | | $ | 34,750 | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Ladner | | | $ | 52,172 | | | | $ | 36,282 | | | | $ | 8,446 | | | | $ | 20,289 | | | | $ | 146,000 | | | | $ | 157,500 | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Martin | | | | None | | | | $ | 9,481 | | | | | None | | | | $ | 9,718 | | | | | None | | | | $ | 51,960 | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| McGill Peterson | | | $ | 52,177 | | | | $ | 36,281 | | | | $ | 8,447 | | | | $ | 20,289 | | | | $ | 151,000 | | | | $ | 152,500 | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Moore | | | $ | 64,625 | | | | $ | 43,069 | | | | $ | 11,083 | | | | $ | 25,405 | | | | $ | 181,000 | | | | $ | 197,000 | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Pruchansky | | | $ | 64,625 | | | | $ | 44,295 | | | | $ | 11,083 | | | | $ | 26,229 | | | | $ | 180,250 | | | | $ | 188,500 | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Compensation for Fiscal Year Ended March 31, 2008

| | | | | | | | | | | |

| Independent Trustee | | | Current Interest | | | | John Hancock Fund Complex* | |

| Carlin | | | $ | 2,139 | | | | $ | 145,250 | |

| Cunningham | | | $ | 1,821 | | | | $ | 145,250 | |

| Jackson | | | | None | | | | | None | |

| Ladner | | | $ | 1,820 | | | | $ | 146,000 | |

| Martin | | | | None | | | | | None | |

| McGill Peterson | | | $ | 1,820 | | | | $ | 151,000 | |

| Moore | | | $ | 2,247 | | | | $ | 181,000 | |

| Pruchansky | | | $ | 2,247 | | | | $ | 180,250 | |

| | | | | | | | | | | |

| |

* | This column reflects the aggregate compensation for each fiscal year end paid to each Trustee from the relevant Trust and from each Fund in the John Hancock Fund Complex that such Trustee serves. The aggregate compensation may include overlapping amounts reflected in the compensation tables for other fiscal year ends. For example, the “Compensation for Fiscal Year Ended May 31, 2008” will reflect aggregate compensation for each month from June 2007 through May 2008. The “Compensation for Fiscal Year Ended August 31, 2008” will reflect aggregate compensation for each month from September 2007 through August 2008. Accordingly, the aggregate compensation paid to each Trustee by the John Hancock Fund Complex from September 2007 through May 2008 will be reflected in both compensation table totals. |

10

Compensation for Fiscal Year Ended May 31, 2008

| | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | John Hancock Fund

| |

| Independent Trustee | | | Bond Trust | | | | Sovereign Bond | | | | Strategic Series | | | | Complex* | |

| Carlin | | | $ | 12,255 | | | | $ | 6,463 | | | | $ | 8,049 | | | | $ | 145,250 | |

| Cunningham | | | $ | 9,924 | | | | $ | 5,335 | | | | $ | 6,595 | | | | $ | 145,250 | |

| Jackson | | | | None | | | | | None | | | | | None | | | | | None | |

| Ladner | | | $ | 9,923 | | | | $ | 5,334 | | | | $ | 6,594 | | | | $ | 146,000 | |

| Martin | | | | None | | | | | None | | | | | None | | | | | None | |

| McGill Peterson | | | $ | 9,924 | | | | $ | 5,334 | | | | $ | 6,594 | | | | $ | 151,000 | |

| Moore | | | $ | 12,370 | | | | $ | 6,588 | | | | $ | 8,188 | | | | $ | 181,000 | |

| Pruchansky | | | $ | 12,370 | | | | $ | 6,588 | | | | $ | 8,188 | | | | $ | 180,250 | |

| | | | | | | | | | | | | | | | | | | | | |

Compensation for Fiscal Year Ended August 31, 2008

| | | | | | | | | | | | | | | | | | | | | |

| | | | California Tax-Free

| | | | Municipal

| | | | Tax-Exempt

| | | | John Hancock Fund

| |

| Independent Trustee | | | Income Fund | | | | Securities Trust | | | | Series Fund | | | | Complex* | |

| Carlin | | | $ | 2,268 | | | | $ | 3,751 | | | | $ | 1,102 | | | | $ | 213,834 | |

| Cunningham | | | $ | 1,652 | | | | $ | 2,721 | | | | $ | 797 | | | | $ | 155,500 | |

| Jackson | | | | None | | | | | None | | | | | None | | | | | None | |

| Ladner | | | $ | 1,652 | | | | $ | 2,721 | | | | $ | 797 | | | | $ | 161,000 | |

| Martin | | | | None | | | | | None | | | | | None | | | | | None | |

| McGill Peterson | | | $ | 1,652 | | | | $ | 1,129 | | | | $ | 797 | | | | $ | 156,000 | |

| Moore | | | $ | 2,097 | | | | $ | 3,463 | | | | $ | 1,016 | | | | $ | 210,000 | |

| Pruchansky | | | $ | 2,173 | | | | $ | 3,596 | | | | $ | 1,057 | | | | $ | 201,500 | |

| | | | | | | | | | | | | | | | | | | | | |

No Trust has a pension or retirement plan for any of its Trustees or officers. Each Trust participates in the John Hancock Deferred Compensation Plan for Independent Trustees (the “Plan”). Under the Plan, an Independent Trustee may elect to have his or her deferred fees invested in shares of one or more funds in the John Hancock Fund Complex and the amount paid to the Independent Trustees under the Plan will be determined based upon the performance of such investments. Deferral of Trustees’ fees does not obligate a Trust to retain the services of any Trustee or obligate the Trust to pay any particular level of compensation to the Trustee. Under these circumstances, the Trustee is not the legal owner of the underlying shares, but does participate in any positive or negative return on those shares to the same extent as all other shareholders. As of December 31, 2008, the value of the aggregate accrued deferred compensation amount from all funds in the John Hancock Fund Complex for Mr. Cunningham was $155,441; Mr. Ladner was $71,250; Ms. McGill Peterson was $112,504; Dr. Moore was $209,776; and Mr. Pruchansky was $255,930 under the Plan.

11

Nominee Ownership of Shares of the Funds

The table below sets forth the dollar range of the value of the shares of each Fund, and the dollar range of the aggregate value of the shares of all funds in the John Hancock Fund Complex overseen or to be overseen by a Nominee, owned beneficially by each Nominee as of December 31, 2008. The table lists only those Funds in which one or more of the Nominees own shares. The current value of the Funds that the participating Independent Trustees have selected under the Plan is included in this table. For purposes of this table, beneficial ownership is defined to mean a direct or indirect pecuniary interest. Exact dollar amounts of securities held are not listed in the table. Rather, the ranges are identified according to the following key:

A-$0

B -$Proposal 1 up to and including $10,000

C -$10,001 up to and including $50,000

D -$50,001 up to and including $100,000

E -$100,001 or more

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | McGill

| | | | | | | | | | | | |

Fund/Trustee | | | Boyle | | | Carlin | | | Cunningham | | | Jackson | | | Ladner | | | Martin | | | Peterson | | | Moore | | | Pruchansky | | | Russo | | | Vrysen |

Balanced

| | | A | | | B | | | C | | | A | | | C | | | A | | | E | | | D | | | D | | | A | | | B |

Bond

| | | A | | | B | | | A | | | A | | | B | | | A | | | C | | | C | | | A | | | A | | | B |

CA Tax Free Income

| | | A | | | A | | | A | | | A | | | A | | | A | | | A | | | A | | | A | | | A | | | A |

Classic Value

| | | A | | | B | | | C | | | A | | | C | | | A | | | B | | | C | | | D | | | A | | | B |

Classic Value II

| | | A | | | B | | | A | | | A | | | A | | | A | | | A | | | A | | | B | | | A | | | B |

Financial Industries

| | | A | | | B | | | A | | | A | | | B | | | A | | | B | | | B | | | B | | | A | | | B |

Global Opp’ty

| | | A | | | A | | | A | | | A | | | A | | | A | | | B | | | A | | | B | | | A | | | B |

Global Real Estate

| | | A | | | B | | | A | | | A | | | B | | | A | | | B | | | B | | | A | | | A | | | B |

Gov’t Income

| | | A | | | B | | | A | | | A | | | B | | | A | | | C | | | B | | | B | | | A | | | B |

Greater China Opp’ty

| | | A | | | B | | | A | | | A | | | B | | | A | | | B | | | A | | | A | | | A | | | B |

Health Sciences

| | | A | | | B | | | A | | | A | | | B | | | A | | | C | | | B | | | B | | | A | | | B |

High Yield

| | | A | | | B | | | A | | | A | | | B | | | A | | | B | | | C | | | B | | | A | | | B |

High Yield Muni Bond

| | | A | | | B | | | A | | | A | | | B | | | A | | | B | | | A | | | A | | | A | | | B |

Intl Classic Value

| | | A | | | B | | | B | | | A | | | C | | | A | | | B | | | A | | | B | | | A | | | B |

Investment Grade Bond

| | | A | | | B | | | A | | | A | | | B | | | A | | | B | | | A | | | B | | | A | | | B |

Large Cap Equity

| | | A | | | B | | | D | | | A | | | B | | | A | | | C | | | D | | | D | | | A | | | B |